You know that feeling, “I’m not saving enough. If I could only win the lottery…” That pressure we put on ourselves is unnecessary and in fact, the system is rigged against us. The financial system itself is intent first on accumulating money, second (or even third) is to make a profit for you.

How The Financial System Delays Retirement

Long-time investment advisor Adam O’Dell spills the beans on his former employers in an article entitled “Why I quit My job as a Financial Advisor” with “…I was expected to toe the company line and only recommend strategies and investments that were “pre-approved,”… Most of the time, that advice centered on “traditional” investment tenets: dollar-cost averaging (read: buying a little more each month), buy-and-hold (err, more like “buy-and-hope!”), asset allocation (but just long stocks and bonds). The odd thing, to me, was that our recommendations in 2008 [, a year of financial crisis,] weren’t all that different from all the years prior. The state of the market seemed to make no difference.”

We spend a lot of money on advisors and money managers. The trick is that they hide the cost in a low sounding management expense ratio (MER) of typically 1-2.5%. So how much is that really? I sat down and figured it out. Because it’s a percentage, we need to consider large sums of money, since the traditional retirement strategy everyone expects is big pot of gold and then taking a few coins out each month to live on. So I started with $100,000 but a more likely figure is several million. Drumroll please!! It costs us around $400-1400/hr (or more!) to pay for these funds and the time it takes to manage the money for you. Most people think twice about paying a professional this much money. Here is a spreadsheet which you can play with yourself. Try changing the number from $100,000 to $1,000,000 or whatever suits your fancy. Click here to access the spreadsheet. This then is why the universal recommendation is to only use a fee-only financial planner. One that doesn’t make commissions or is motivated to put you in funds that charge an MER.

Further digging into the spreadsheet mentioned, it tells us why that Mutual Fund or Exchange Traded Fund (ETF) basically treads water. Take that traditional retirement model; the big pot of gold. How many coins can we take out of it each year? Called “a safe withdrawal rate” my research indicates a reasonable amount is 2%. Remember, the fund is charging you the MER in retirement and also in situations where the fund loses money. So add the MER and the safe withdrawal rate together and you have a significant negative trend against building wealth.

The Single Best Investment (AKA “Dividend Achievers”)

There is a better way…. Something I stumbled on to. It has a significant history of success dating right back to the start of the stock exchange in 1602. Mr. Lowell Miller introduced the concept to me in his book, now a free PDF online, called “The Single Best Investment: Creating Wealth with Dividend Growth.” (It is also on amazon if you want to pay for the e-book or buy an old paper copy. Also, there are copies at most public libraries.)

Single Best Investment has also been called the “dividend achievers” strategy and is one of the few (only?) proven long term buy and hold strategies that work. What is it? Basically it is an investment in stocks that have raised their dividend every year. Meaning the investment is not for the dividend itself but the dividend growth rate. Click here for more on “dividend achievers”.

How the Single Best Investment Works

It works because it does two critical things:

- eliminates financial fees

- focuses money in companies that stay healthy with very low risk of long term downside

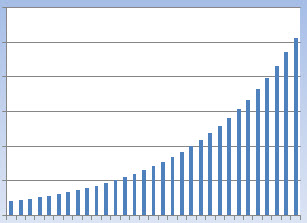

Because it is based on a growth rate for dividends, there is a “hockey stick” compounding growth graph. (You can learn more about “Payback, RoI, IRR” by clicking here.)

- Simple, minimal maintenance strategy

- Focuses on key factors important to personal financial situations: cash flow, safety

- Still grows if cash flow not reinvested

- Cash flow increases through retirement

- Can eliminate the need to continuously save for retirement

- Supports “rewirement”

- Qualifies for debt interest deductibility (an advanced tax strategy)

Congratulations! You Care About Your Money!

If you made it the bottom of this article, congratulations. You are one of the few people who cares that your money makes money. Not many people do. North American society has all sorts of funny money myths, and collectively we subconsciously do not think we deserve it. Have you ever tried to talk to a fellow North American about money? You’ll see.

So what do I do? I have documented my experience and tools to help bootstrap people. Most people tell me they “don’t have the skills to invest themselves” but most people already do tasks many times more complex than investing. To list the required skills a person needs to know how to read, multiply, divide and handle percentages.

Next Steps

I offer a 3 hour introductory course (contact me here) and pay as you go coaching for people not inclined to read the book and do-it-themselves. To date, no one has ever needed more than 4 hours total. It is that easy. The strategy requires some time to setup, but then it’s “set it and (mostly) forget it”; just like buy and hold should be. For those who do not have much seed money and want to know what tools are available to help accelerate their progress, I offer an additional advanced course. If you think investing and saving is way beyond your lifestyle, consider that people making poverty line incomes have successfully used this strategy. That’s one of the many money myths.

About my involvement as a coach: I don’t make enough money from this for it to be anything but a hobby that makes a little money. The other reason I charge is because we can’t have a contract that places the responsibility for investing on the investor without doing so. The reason I coach is because I believe it benefits people. What I don’t do is provide motivation for conducting the strategy although I do discuss the psychological hurdles as part of the course. The psychology and the motivation are the hard part and finding tools for overcoming that comes from countless motivational materials available at any book store or library.

Happy Investing,

Trevor

2 Replies to “The Single Best Investment – Avoiding the Doomed Retirement Feeling”